Futures Market: Overnight, LME copper opened at $9,124.5/mt, hitting a high of $9,131.5/mt at the beginning of the session before fluctuating downward, bottoming at $9,063.5/mt during the session. It then rebounded and maintained slight fluctuations towards the end, finally closing at $9,094/mt, up 0.23%. Trading volume reached 16,000 lots, and open interest stood at 276,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,510 yuan/mt, initially declining to a low of 75,140 yuan/mt before rebounding to a session high of 75,520 yuan/mt. Towards the end, the center of gravity shifted downward amid fluctuations, closing at 75,320 yuan/mt, down 0.13%. Trading volume reached 20,000 lots, and open interest stood at 144,000 lots.

【SMM Copper Morning Brief】News: (1) In response to questions regarding the US's release of export control measures on artificial intelligence, a spokesperson for China's Ministry of Commerce stated that China has taken note of the Biden administration's announcement on January 13 regarding AI-related export controls and firmly opposes it. (2) Recently, market rumors suggested that the central bank, in collaboration with the CSRC and CFFEX, is investigating irregularities and alleged manipulation in treasury futures trading. It was also rumored that CFFEX was instructed to raise margin requirements and fees for treasury futures to curb speculative trading. However, according to relevant authorities, these rumors are unfounded.

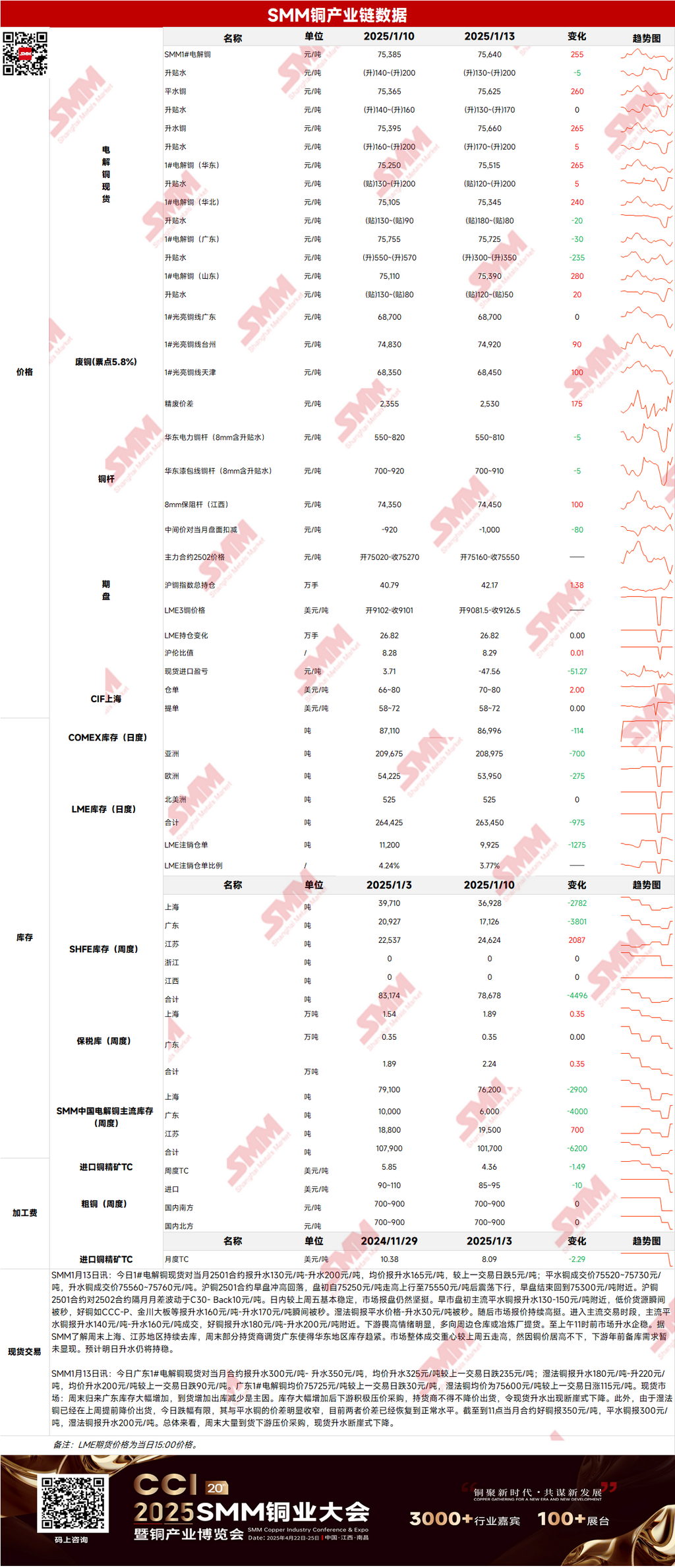

Spot Market: (1) Shanghai: On January 13, #1 copper cathode spot premiums against the front-month 2501 contract were quoted at 130-200 yuan/mt, with an average of 165 yuan/mt, down 5 yuan/mt WoW. According to SMM, inventories in Shanghai and Jiangsu continued to decline over the weekend, with some suppliers transferring goods to Guangdong, tightening inventories in east China. Overall, the market's trading center shifted higher compared to last Friday. However, due to high copper prices, pre-holiday stocking demand from downstream buyers has yet to emerge. Spot premiums are expected to remain stable today.

(2) Guangdong: On January 13, #1 copper cathode spot premiums against the front-month contract were quoted at 300-350 yuan/mt, with an average of 325 yuan/mt, down 235 yuan/mt WoW. Over the weekend, significant arrivals led to downstream buyers bargaining down purchasing prices, causing spot premiums to plummet.

(3) Imported Copper: On January 13, warehouse warrant prices were $70-80/mt, QP January, with an average up $2/mt WoW. B/L prices were $58-72/mt, QP February, with the average unchanged WoW. EQ copper (CIF B/L) was quoted at $6-20/mt, QP February, with the average unchanged WoW. Quotes referenced cargoes arriving in mid-to-late January and early February. Yesterday, the SHFE/LME price ratio remained flat compared to last Friday, with limited market offers and muted transactions. Demand was mainly focused on cargoes arriving in early-to-mid February and bonded warehouse warrants.

(4) Secondary Copper: On January 13, secondary copper raw material prices remained unchanged WoW. Guangdong bare bright copper prices were 68,600-68,800 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 2,530 yuan/mt, up 175 yuan/mt WoW. The price spread between primary and secondary copper rods was 1,680 yuan/mt. According to SMM surveys, the price difference between primary metal and scrap continues to widen. Domestic secondary copper raw material prices saw limited increases due to insufficient demand from secondary copper rod enterprises. With few post-holiday orders, these enterprises are reluctant to stockpile excessive secondary copper raw materials for the holiday, resulting in low quotes.

(5) Inventory: On January 13, LME copper cathode inventories decreased by 975 mt to 263,450 mt. SHFE warehouse warrant inventories decreased by 1,455 mt to 11,085 mt.

Prices: Macro side, the New York Fed survey showed a one-year inflation expectation of 3%. Traders priced in less than a 25-basis-point interest rate cut by the US Fed this year. The US dollar index pulled back significantly, while crude oil prices surged consecutively, providing support to copper prices. Fundamentals side, some suppliers transferred goods to Guangdong over the weekend, with inventories in Shanghai and Jiangsu continuing to decline, tightening supply in east China. The trading center for copper cathode shifted higher compared to last Friday. However, high copper prices have yet to stimulate pre-holiday stocking demand. Overall, with the US dollar index pulling back from highs and crude oil prices rising, copper prices are expected to receive some support today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make cautious decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】